What is Money Purchase Annual Allowance 2025?

In recent years, more people have begun accessing their pensions flexibly to support a phased retirement or supplement their income. However, this increased flexibility brings with it a set of complex tax rules one of the most important being the Money Purchase Annual Allowance (MPAA).

In 2025, understanding how this allowance operates is vital for anyone drawing from or contributing to a defined contribution pension.

The MPAA can significantly reduce how much you can save tax-efficiently into your pension if you’ve already started taking money from it. This article outlines what the MPAA is, how it works in 2025, when it’s triggered, and what actions you should take to avoid any costly tax implications.

What Does the Money Purchase Annual Allowance (MPAA) Mean in 2025?

The Money Purchase Annual Allowance (MPAA) is a rule introduced by the UK government in 2015 to limit how much you can contribute to defined contribution pensions once you begin to take taxable income from them.

The aim is to prevent individuals from taking money out of their pension, benefiting from tax relief, and then reinvesting it straight back into the pension to gain additional tax advantages.

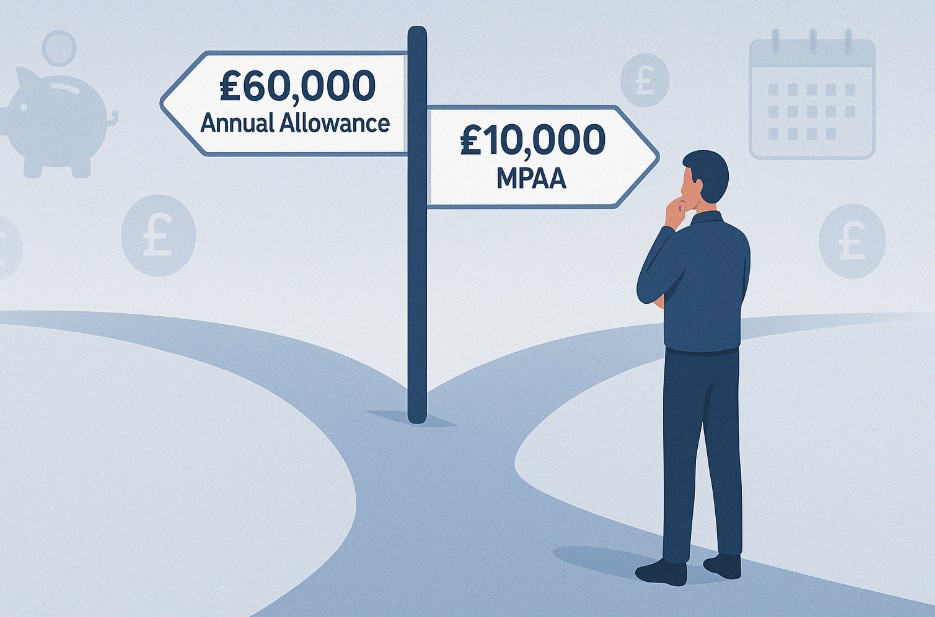

In the 2025/26 tax year, the MPAA remains at £10,000 per year, a figure reinstated in 2023 after a period of being just £4,000.

This reduced allowance applies to anyone who has accessed their pension flexibly and covers the total contributions from both the individual and their employer across all defined contribution schemes.

To continue receiving tax relief on pension contributions, two conditions must be met:

- The total contributions (yours and your employer’s combined) must not exceed the MPAA.

- Your personal contributions must not exceed your annual earnings.

The MPAA is separate from and lower than the standard annual allowance, which is currently £60,000 in the 2025/26 tax year. If you haven’t triggered the MPAA, you’re entitled to contribute up to this higher limit, assuming your earnings allow.

How It Works with Low Income?

If you earn under £3,600, you can still receive tax relief on pension contributions of up to £3,600 annually. This equates to £2,880 of your money and £720 of tax relief.

What Are the Key Changes to MPAA in 2025?

While the MPAA threshold has not changed for the 2025/26 tax year and remains at £10,000, it’s essential to recognise how this rule continues to shape pension strategies.

If you trigger the MPAA partway through a tax year, the timing affects how much you can contribute under the standard annual allowance versus the MPAA.

Any pension contributions made before the trigger event are assessed against the £60,000 standard allowance, while those made after the trigger are assessed against the £10,000 MPAA.

This means you must be mindful of your pension activity throughout the year to avoid breaching the applicable limit, especially if you continue to work and contribute to your pension after drawing from it.

How Is the MPAA Different from the Standard Annual Allowance?

The standard annual allowance is the total amount of pension contributions eligible for tax relief in any tax year, set at £60,000 for 2025/26.

This allowance applies to both defined contribution and defined benefit pension schemes and allows for the carry-forward of unused allowance from the previous three years.

The MPAA, on the other hand, is much more restrictive. It applies only to defined contribution schemes and only if you have flexibly accessed your pension. Unlike the standard allowance, the MPAA:

- Does not allow you to carry forward unused allowances.

- Cannot be reversed once triggered.

- Is permanently applied in all future tax years after the initial trigger.

This significantly limits the flexibility you have for tax-efficient saving into pensions after accessing your retirement funds.

What Triggers the Money Purchase Annual Allowance in 2025?

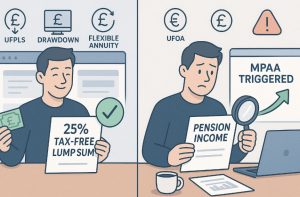

The MPAA is only triggered when you take taxable income from a defined contribution pension.

Simply taking your tax-free cash entitlement usually up to 25% of your pot, does not trigger the MPAA as long as the rest remains invested or used to buy a guaranteed income product like a lifetime annuity.

The MPAA will normally be triggered if:

- You start taking income via flexi-access drawdown.

- You withdraw a series of UFPLS (Uncrystallised Funds Pension Lump Sums).

- You cash in your entire pension as a lump sum (excluding small pots under £10,000).

- You exceed the income limit on a capped drawdown plan.

- You purchase a flexible or investment-linked annuity where income levels can decrease.

Conversely, actions that do not usually trigger the MPAA include:

- Withdrawing only the 25% tax-free lump sum and deferring income.

- Buying a lifetime annuity with a guaranteed income.

- Taking money from a defined benefit (final salary) pension.

If you’re unsure whether your pension counts as defined contribution or defined benefit particularly in the case of AVCs (Additional Voluntary Contributions), it’s best to confirm with your scheme provider before withdrawing funds.

How Does the MPAA Affect Pension Contributions?

Once triggered, the MPAA limits your total annual defined contribution pension savings to £10,000 including both personal and employer contributions. If you exceed this amount, you’ll be required to pay tax on the excess.

This can significantly affect savers who wish to continue contributing to pensions while drawing income from them, especially those still in part-time or full-time work. It may also impact individuals looking to make large one-off contributions before retirement.

The loss of the ability to carry forward unused annual allowance means you have much less flexibility in managing your pension savings across tax years.

How Does the MPAA Affect Your Pension Tax Relief?

Tax relief is still available for contributions within the MPAA, but anything above the £10,000 threshold is not eligible for relief and will be taxed at your marginal rate.

Let’s consider an example: Jill contributes £1,000 per month to her pension. On 1 November 2025, she makes a taxable withdrawal from her pension, which triggers the MPAA. Contributions made before November are assessed against the £60,000 annual allowance.

From November onwards, only £10,000 of annual contributions are permitted. If Jill continues contributing at the same rate, she’ll exceed the MPAA by £5,000, leading to an additional tax charge.

Tax charges for exceeding the MPAA must be declared via Self Assessment. In some cases, you can request your pension provider to pay this tax on your behalf under the scheme pays option, although this is typically only mandatory for charges above £2,000.

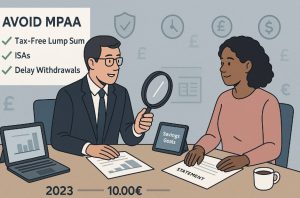

What Can You Do to Avoid or Manage the MPAA?

If you’ve not yet triggered the MPAA, careful planning can preserve your ability to contribute up to £60,000 annually.

Strategies include:

- Avoiding or delaying taxable withdrawals from your defined contribution pension.

- Taking only the tax-free lump sum while deferring further income.

- Using ISAs or other investment vehicles to build your retirement fund without impacting pension limits.

If the MPAA has already been triggered, you must plan within the £10,000 limit and consider shifting surplus income into other savings methods. Consulting a regulated financial adviser is strongly advised to avoid mistakes and potential tax charges.

How Can You Plan Your Pension in 2025 With the MPAA in Mind?

Proactive pension planning is crucial if you intend to access your pension while continuing to contribute to it. This is especially relevant for those transitioning into retirement gradually or returning to work after partial retirement.

If you’re contributing to both a defined contribution and a defined benefit pension:

- The MPAA still limits your defined contribution contributions to £10,000.

- You may still receive tax relief on the annual growth of your defined benefit scheme, up to the alternative annual allowance (normally £50,000 if your defined contribution contributions remain within the MPAA).

If you don’t contribute to defined contribution pensions at all, your defined benefit pension can grow up to the standard £60,000 allowance.

Conclusion

The Money Purchase Annual Allowance is a permanent rule that affects anyone who begins to draw taxable income from a defined contribution pension. Once triggered, it restricts your total annual contributions to £10,000 across all such pensions.

It is vital to:

- Understand what actions will trigger the MPAA.

- Monitor your contributions post-trigger to avoid breaching the limit.

- Notify all providers of your MPAA status within 91 days.

- Factor the MPAA into your long-term retirement planning.

Failing to comply with these requirements can result in financial penalties and unexpected tax bills. For these reasons, seeking advice from a qualified financial professional is often the best course of action.

Frequently Asked Questions (FAQs)

Does the MPAA apply to final salary pensions?

No, the MPAA only applies to defined contribution pensions. Final salary or career average schemes are not affected.

Can I still receive tax relief if I’ve triggered the MPAA?

Yes, but only on contributions up to the MPAA limit of £10,000 annually.

How will I know if the MPAA has been triggered?

Your pension provider is required to inform you with a flexible access statement within 31 days of a trigger event, or 91 days for overseas pensions.

What happens if I exceed the MPAA?

You’ll be liable for an annual allowance tax charge and must report this via your Self Assessment tax return.

Can I offset excess contributions with unused allowances from earlier years?

No, the MPAA does not allow carry forward of unused allowance.

Do I need to notify other pension providers if I trigger the MPAA?

Yes, you must inform all other providers within 91 days of receiving notification to avoid a fine.

Is professional advice recommended?

Absolutely. The MPAA rules are complex and impact your retirement strategy. A qualified financial adviser can help you navigate them effectively.